For giggles, lets skip forward “a few miles into the marathon.” You’ve finished college (with little or no debt to repay, right?) and you’ve found a career that both motivates you and pays fairly well. Congrats! All of a sudden, you’ve gone from being a poor college student who’s scraping by every week to having what seems like a boatload of money in your pocket and you feel rich!

The sudden increase in the amount of money you have coming in may tempt you to “pick up the pace” like some of your friends will almost certainly do when they see those first paychecks. A new car, a fancy new apartment…..maybe a big increase in your entertainment budget every week.

This is the point in the Money Marathon where you as a smart game planner with a long-term goal will set yourself apart from the pack. These big new expenses might be in your friend’s plans, but you sense that they really might run you right into a Pit of Pain. What exactly is the right thing to do? Following our marathon analogy, I’ll just tell you that you’ll want to save as much of this new found energy as possible for the long road ahead.

“Great, Dad. That’s really helpful. How much is ‘as much as possible?'” you are probably saying to yourself.

The truth is, there is no one specific percentage of your income to save that is right for everyone and its always somewhat dependent upon your individual circumstances (where you live, how much you make, etc). Your Pops, however, isn’t wishy-washy and these posts are mostly about providing actionable content, so let’s just draw a line in the sand to start with…

- 10% of your gross income should go to pre-tax retirement contributions

- 20% of your take home pay should go to post-tax savings for investment

These are the minimums you want to be saving for investment, especially for the take-home pay savings. If you can practically save more, do it.

Pay Yourself First!

Don’t worry too much right now about what terms like gross income, pre-tax, post-tax and take home mean. We’ll eventually get into them. Just commit to the notion of saving first and note that what you are doing by setting aside a portion of your income before you consider how much you have to spend on food, shelter, and fun is really paying yourself first. This is because the money you save now, properly invested, will go to work for you increasing your net worth relatively passively while you live your life. You see, your greatest ally right now early in the Money Marathon is time. Well, time and something called compound interest.

“Compound interest is the 8th wonder of the world […].”

Albert Einstein

Your Pops gets no originality points for using this quote attributed to Albert Einstein. As you pick up interest (a pun!) in personal finance and begin scanning the Web for far better content than anything I can cobble together, you will certainly find this quote referenced hundreds of times. I decided to use it anyway because a dude as brilliant as Einstein, who came up with some pretty amazing concepts himself, found the math behind how money multiplies over time with compounded returns to be wondrous.

You don’t have to dig into all the math behind it, though if you’d like to here’s a link to one decent explanation. What’s important to understand now is that by committing to saving first and investing your savings effectively for the long haul your money will do a wondrous job of making more money for you. How much more? Well…consider the following somewhat silly scenarios, that hopefully make the point:

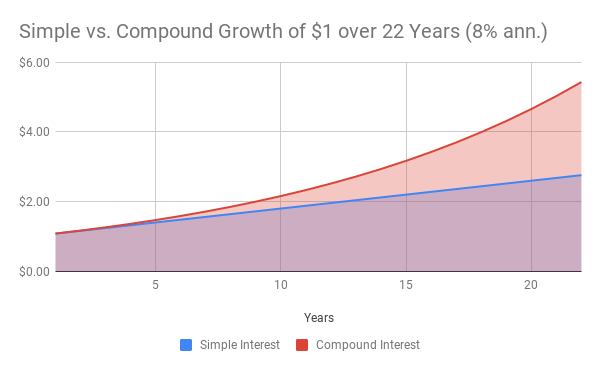

Let’s say you save exactly $1 from your first paycheck after graduating from college. You take that dollar and invest it in a *theoretical bank account that pays 8% annual interest and you leave it there for the remaining 22 years (assuming you graduated from college in 4 years) of your Money Marathon. For simplicity, assume that buck earns a 8% annual return each and every year and that you leave your original $1 invested, but you take that money you earn each year (the interest) out of the account and stick under your mattress for safekeeping. How much do you think you’ll have in interest under your mattress in 22 years?

$1.76.

That’s right. You put a $1 in, let it sit invested, and you got back $.08 (8%) each year for 22 years. You now have $2.76 if you count the original $1 you left invested.

“Wow Dad, that’s really amazing. I have no idea what I’m going to do with that $2.76 in 22 years!”

“Unimpressed, eh?”

You’re right, you probably aren’t getting rich, but do keep in mind that it is a 176% total return on your original $1. While you did nothing but make your initial investment and pulled the earnings out once a year to stick them under your mattress, your money nearly tripled. It’s better than spending that buck on a cup of coffee on your 1st day of work, which will be worth absolutely nothing to you 22 years from now. It’s also not an example of compound interest! Its an example of simple interest, and there’s a reason Einstein wasn’t enamored of simple interest.

So let’s get back to compound interest…

Say you follow the same scenario of investing $1 from your very first paycheck in the same bank account to earn the same 8% annual return. However, this time instead of pulling each year’s earnings out and sticking it under your mattress, you leave it in the account to earn it’s own 8% return, compounding your return in future years too. And say you just keep doing that every single year with the earned interest. Now guess how much you’ll have after 22 years?

$5.44

To be clear, that’s the original $1 + $4.44 in interest earned with compounding and time. You may still be less than impressed by ending up with enough dough for a couple Chipotle tacos, but think about this a bit. That dollar you invested 22 years ago and left alone to grow in the bank is now worth 444% more than the original $1 and almost 2X the amount you’d have with the simple return approach.

To further illustrate the power of compounding over simple returns, you’d have to earn a 20% return a year with simple interest ($0.20 x 22 years = $4.44) to match the performance of the turbocharged, compounded 8% returns. And, believe me when I say that 8% compounded returns are a totally achievable while 20% simple returns are unheard of. It just ain’t happenin’.

That, my dearies, is what makes compound interest a wondrous bit of math, and all you need to take advantage of it is a commitment to saving, some common sense, patience in investing and time. And, because you are young Money Marathoners, you have all of these tools in your game plan. Sweet!

Now lets get serious about savings and compound returns.

What if, instead of saving just one time with your 1st paycheck, you committed to faithfully saving and investing 10% of your gross income and 20% of your take-home pay every single paycheck for the remaining 22 years of the Money Marathon. How much do you think you’d have then?

For now, I’ll just tell you that it’s a boat load. Play it right and stick to the plan, and it likely will be north of $1 million!

That’s right…little ‘ol you with even a modest income has a pretty decent chance of becoming a millionaire before you are 45 years old just by being committed to paying yourself first through savings and investing the savings smartly. The more you save, the faster you’ll be a millionaire and reach the Money Marathon finish line. Start out with 10% of your pre-tax and 20% of your post-tax as the lowest percentages of your income you’ll reserve for savings and investment, and then strive to drive it higher as your earnings increase with time.

Of course, you might be wondering if you can save all this money and still have enough money to pay for your required living expenses as well as some fun. I’ll be honest…It isn’t going to be easy. You have to be committed and willing to keep close tabs on what you spend your money on. This is where understanding how much money you have coming in and how much you are paying out is important, and this is the topic for our next few posts.

One thought on “#6 -Pay Yourself First with Savings”